AICPA & Beyond: Navigating Health Insurance Options for Accounting Professionals

Health insurance for accountants is more than just another expense—it's a critical component of financial security and long-term career sustainability. Whether you're a self-employed CPA, work at a small firm without group benefits, or simply need to evaluate your current coverage, understanding your options is essential for protecting both your health and your financial future.

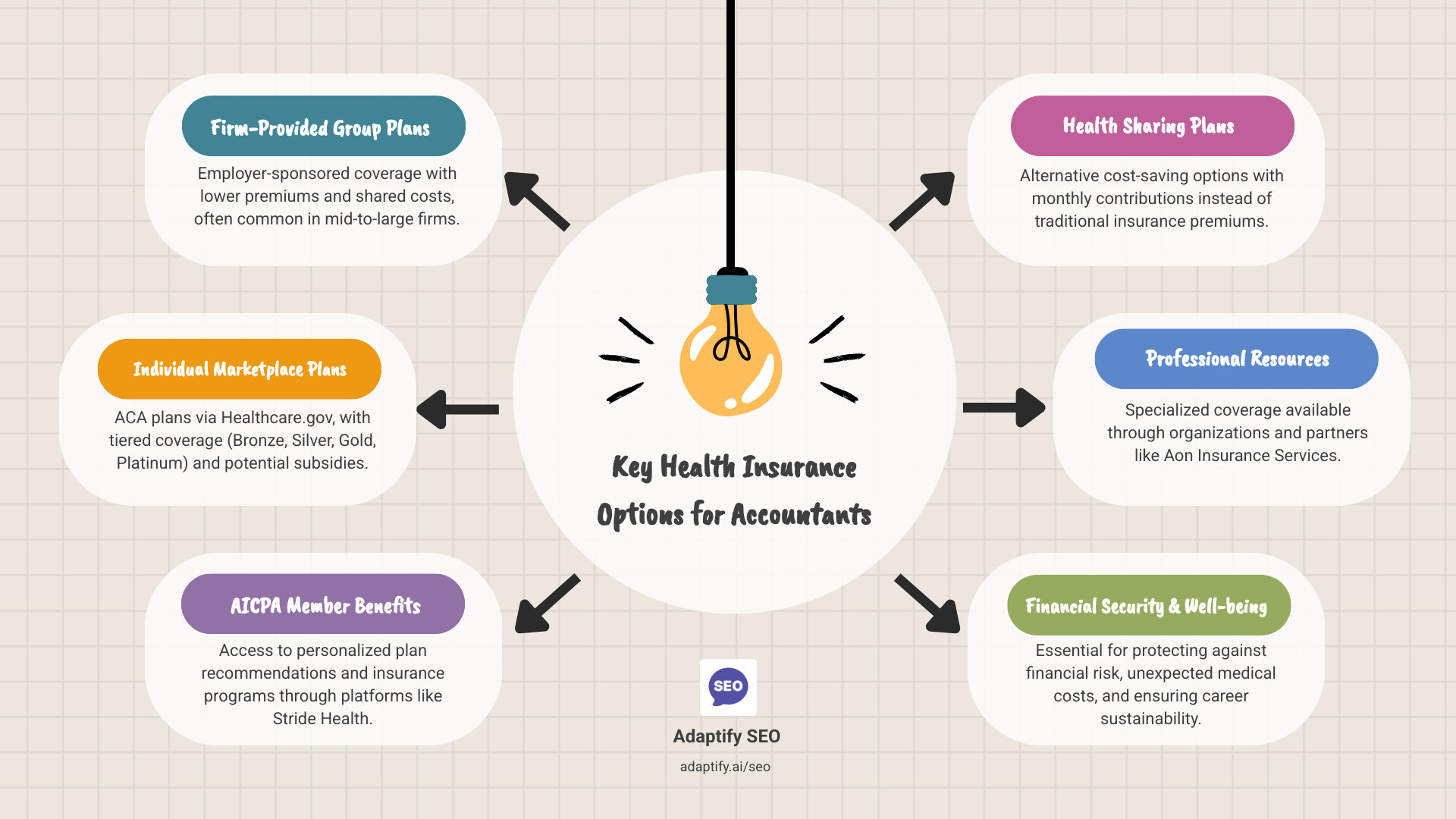

Key Health Insurance Options for Accountants:

The stakes are higher than many accounting professionals realize. According to the Kaiser Family Foundation, average annual health insurance premiums hit $7,911 for single coverage and $22,463 for family coverage as of 2024, before Affordable Care Act subsidies. Meanwhile, deductibles have skyrocketed—from around $1,217 in 2014 to an average of $7,481 for Bronze plans in 2023. For self-employed accountants and those at smaller firms without group benefits, navigating these costs while finding adequate coverage can feel overwhelming.

The accounting profession also faces unique health considerations. With 2,900 workplace injuries reported within the accounting industry in 2018—many related to repetitive strain and poor ergonomics—and the intense stress of tax season, having comprehensive health coverage isn't just about routine care. It's about protecting yourself from both the physical demands of desk work and the mental health challenges that come with managing client finances and meeting tight deadlines.

While our primary expertise is in product design and marketing for SaaS platforms, we've worked extensively with financial services companies and understand the importance of comprehensive planning for accounting professionals seeking health insurance for accountants. Through this guide, we'll help you steer the complex landscape of coverage options so you can make informed decisions that protect both your health and your bottom line.

As an accounting professional, you spend your days helping clients manage their finances, minimize risk, and plan for the future. But how much attention do you give to your own financial well-being, particularly when it comes to healthcare? Unexpected medical costs can derail even the most carefully crafted financial plans. This is why health insurance for accountants isn't just a good idea; it's an absolute necessity.

The financial risk of being uninsured or underinsured is staggering. A sudden illness, an accident, or even a chronic condition can quickly lead to medical bills that wipe out savings, jeopardize retirement plans, and force difficult financial choices. For self-employed accountants, this risk is amplified, as there's no employer safety net to catch them.

Beyond the financial aspect, accountants face specific health needs. Long hours spent hunched over a desk, meticulous data entry, and the high-pressure environment of tax season can take a toll. Sedentary work can lead to musculoskeletal issues, while the mental strain can contribute to stress, anxiety, and burnout. Comprehensive health coverage provides access to preventative care, specialist consultations, and mental health support, all crucial for maintaining your well-being and, by extension, your career longevity.

The rising cost of health insurance is a stark reality. According to the Kaiser Family Foundation, average annual health insurance premiums hit $7,911 for single coverage and $22,463 for family coverage as of 2024, before Affordable Care Act subsidies are taken into account. These numbers underscore the importance of finding smart, cost-effective solutions.

Having robust health insurance for accountants provides immense peace of mind. It allows you to focus on your work, your clients, and your life, knowing that you're protected against the unforeseen. It's also vital for business continuity; a healthy accountant is a productive accountant.

Let's talk numbers, because that's what accountants do best, right? The statistics from the Kaiser Family Foundation are sobering: average annual health insurance premiums hit $7,911 for single coverage and $22,463 for family coverage as of 2024. These are just the premiums! Then there are the deductibles, which have seen a dramatic increase. In 2014, the average deductible for a single person was around $1,217. By 2023, average deductibles had risen to $7,481 for Bronze plans, $4,890 for Silver plans, $1,650 for Gold plans, and $45 for Platinum plans.

Imagine facing a medical emergency with a Bronze plan deductible of nearly $7,500. That's a significant chunk of change, even for a financially savvy accountant. Without adequate coverage, these costs can quickly escalate, forcing you to dip into your emergency fund, take on debt, or even liquidate investments. This directly impacts your ability to protect personal assets and achieve your long-term financial goals, whether that's saving for retirement, buying a home, or funding your children's education. Health insurance acts as a crucial barrier, shielding your hard-earned assets from the unpredictable high costs of healthcare.

While accounting might not be as physically demanding as, say, construction, it comes with its own set of unique health challenges. The sedentary nature of desk work, coupled with repetitive tasks like typing and data entry, makes accountants particularly susceptible to certain conditions.

Consider repetitive strain injuries (RSIs) like carpal tunnel syndrome, which can be debilitating and require extensive treatment, including physical therapy or even surgery. The research shows that in 2018, there were 2,900 workplace injuries within the accounting industry. Many of these are likely related to ergonomics and repetitive motions. Ensuring your health plan covers these types of treatments, including specialists and rehabilitation, is crucial.

Beyond physical ailments, the mental toll of the accounting profession, especially during peak seasons like tax time, can be immense. Long hours, tight deadlines, and the pressure of managing sensitive financial data can lead to stress, anxiety, and burnout. A good health insurance plan should offer robust mental health support, including therapy, counseling, and psychiatric services, to help you manage these pressures and maintain your overall well-being. Preventing burnout isn't just good for you; it's good for your clients and your business too.

Navigating health insurance can feel like trying to balance a complex ledger – lots of numbers, terms, and regulations to understand! But don't worry, we're here to simplify it for you. The type of health insurance available to you often depends on your employment status. Let's break down the main options.

For many accountants working in established firms, group health insurance is the most common and often the most advantageous option. These plans are sponsored by your employer and typically offer a range of benefits.

The primary benefits of group plans include generally lower premiums compared to individual plans, because the risk is spread across a larger pool of employees. Employers also often subsidize a significant portion of the premium, further reducing your out-of-pocket costs. Group plans also tend to have broader networks of doctors and specialists and may offer more comprehensive coverage.

When evaluating your employer's options, look beyond just the monthly premium. Consider the deductible, copayments, coinsurance, and the annual out-of-pocket maximum. Also, check the plan's network to ensure your preferred doctors and hospitals are included. These plans are common for mid-to-large size firms and often extend coverage to your spouse and dependents, which is a huge plus for family planning.

If you're a self-employed accountant, work for a small firm that doesn't offer group benefits, or are between jobs, individual health insurance plans are your go-to. The primary avenue for these plans is through the Affordable Care Act (ACA) marketplaces, often referred to as Healthcare.gov or your state's specific marketplace.

The ACA marketplace offers a standardized way to compare plans, which are categorized into "metal tiers":

One of the biggest advantages of the ACA marketplace is the availability of subsidies and tax credits. These financial aids can significantly reduce your monthly premiums, making coverage much more affordable, especially for those with moderate incomes. It's important to apply for these subsidies during enrollment to see what you qualify for.

Understanding when you can enroll in a health insurance plan is just as important as understanding the plans themselves. There are two main periods you need to be aware of:

Here's a list of common Qualifying Life Events:

If you experience any of these events, make sure to act quickly to take advantage of your SEP. It's your opportunity to get coverage when you need it most.

Finding the right health insurance for accountants isn't just about picking a plan; it's also about leveraging available resources and exploring alternatives that might better suit your unique financial situation.

As an accounting professional, you're likely aware of the value of professional organizations. The AICPA (American Institute of Certified Public Accountants) is a prime example, offering a range of resources, including insurance programs. The AICPA Member Insurance Programs, in partnership with Aon, provides members with access to various insurance solutions custom for CPAs.

Specifically for individual health insurance, the AICPA endorses and partners with Stride Health. The Stride Health platform is a fantastic resource for members, their spouses, parents, and friends. It's free to use and designed to simplify the complex process of finding individual health insurance coverage.

Here's what Stride Health offers:

To get started, we highly recommend visiting the Stride Health platform to find available plan options. It's a powerful tool to help you find the plan that works best for your needs, budget, and personal preferences.

When considering health insurance for accountants, it's important to look at all avenues, including alternatives to traditional insurance. Health sharing plans have gained traction as a potentially cost-effective option, particularly for self-employed individuals and small business owners. But what exactly are they, and how do they compare?

Let's lay out the differences:

| Feature | Traditional Health Insurance | Health Sharing Plans |

|---|---|---|

| Regulation | Regulated by state and federal laws (e.g., ACA, HIPAA) | Not regulated as insurance; exempt from ACA mandates |

| Coverage | Legally bound to pay covered claims; mandated benefits (e.g., maternity, mental health) | Members "share" medical costs based on agreed-upon guidelines; not a legal guarantee of payment |

| Cost | Monthly premiums; often higher, especially without subsidies | Monthly "contributions" or "shares"; often lower than unsubsidized premiums |

| Network | Typically use PPO, HMO, EPO networks with contracted providers | Often no network restrictions, allowing choice of any provider |

| Pre-existing Conditions | Must cover pre-existing conditions after a waiting period (ACA-compliant plans) | May have waiting periods or exclusions for pre-existing conditions |

| Tax Deductibility | Premiums may be tax-deductible for self-employed individuals | Contributions are generally not tax-deductible |

Health sharing plans are typically offered by health sharing ministries, where members with similar ethical or religious beliefs contribute to a common fund to help cover each other's medical expenses. The appeal often lies in the lower monthly contributions.

For example, a self-employed consultant could switch to a health sharing plan costing $350 per month ($4,200 annually) from an unsubsidized health insurance plan that cost $700 per month ($8,400 annually), saving $4,200 each year. Even after factoring in tax deductibility for traditional health insurance premiums (assuming a 22% tax bracket), the net cost for traditional insurance would be around $6,552, while the net cost for the health sharing plan would remain $4,200. This hypothetical example highlights the potential savings.

However, it's crucial to understand that health sharing plans are not traditional insurance. They are not legally bound to pay claims, may not cover all types of care (like preventative services or mental health), and often have limitations or waiting periods for pre-existing conditions. While they can be a viable option for healthy individuals seeking lower costs, we strongly advise thorough research into the specific plan's guidelines, limitations, and the ministry's track record before committing.

While health insurance takes center stage, a comprehensive risk management strategy for accountants extends beyond medical care. As a professional who deals with financial security, you know the importance of protecting all aspects of your livelihood.

Thinking holistically about your insurance needs means building a layered defense against various risks, ensuring your personal and professional finances remain secure.

As an accountant, you're an expert at managing budgets and forecasting financial outcomes. Applying that same rigor to your health insurance decisions is key to finding affordable, effective coverage.

Several factors play a significant role in determining how much you'll pay for your health insurance for accountants:

Understanding these factors allows you to anticipate costs and make more informed choices when comparing plans.

One of the smartest ways to manage health insurance costs, especially for self-employed accountants, is to leverage available tax benefits.

The goal is to find a plan that provides adequate coverage without breaking the bank. This often involves a careful balancing act between premiums and deductibles.

Navigating the complex world of health insurance for accountants might seem daunting, but as we've outlined, there are numerous options and strategies to ensure you're well-covered. We've explored why health insurance is a non-negotiable for accounting professionals, dug into the specifics of firm-provided, individual, and marketplace plans, and even considered alternatives like health sharing. We've also touched on the critical role of AICPA member benefits and platforms like Stride Health in simplifying your search, and discussed how to integrate health insurance into your broader financial and tax planning.

Your health is truly your most valuable asset, and protecting it with appropriate insurance is one of the smartest investments you can make. Just as you advise your clients to plan for their financial future, we encourage you to be proactive in planning for your own healthcare needs. Don't wait for a medical emergency to highlight the gaps in your coverage.

Take control of your coverage today. Explore the options, compare costs, and choose a plan that safeguards your well-being and aligns with your financial goals. And if you're looking to grow your accounting practice and reach more clients who need your financial expertise, a strong online presence is key.

Explore our SEO services to grow your practice to see how Adaptify SEO can help you connect with more potential clients and build a thriving business.

Streamline content creation & boost ROI with Marketing content automation. Discover AI's role, best practices, and top tools to scale your...

Discover how AI Powered Outreach automates link building with 3x more placements and 96% efficiency gains in 2026.

Discover how journalist outreach software replaces mass pitching with AI-powered, personalized media pitches that boost response rates and...

Join 1,000+ agencies already delivering SEO and AI visibility from a single platform without increasing their headcount.Join 1,000+ agencies already delivering SEO and AI visibility from a single platform without increasing their headcount.