Blueprint for Wellness: Navigating Health Insurance for Engineers

Health insurance for engineers isn't a one-size-fits-all topic. Whether you work at a small three-person civil engineering firm, consult independently as a chemical engineer, or move between employers every few years, your coverage needs are genuinely different from those in most other fields.

Here's a quick overview of the main ways engineers can get covered:

| Option | Best For | Key Benefit |

|---|---|---|

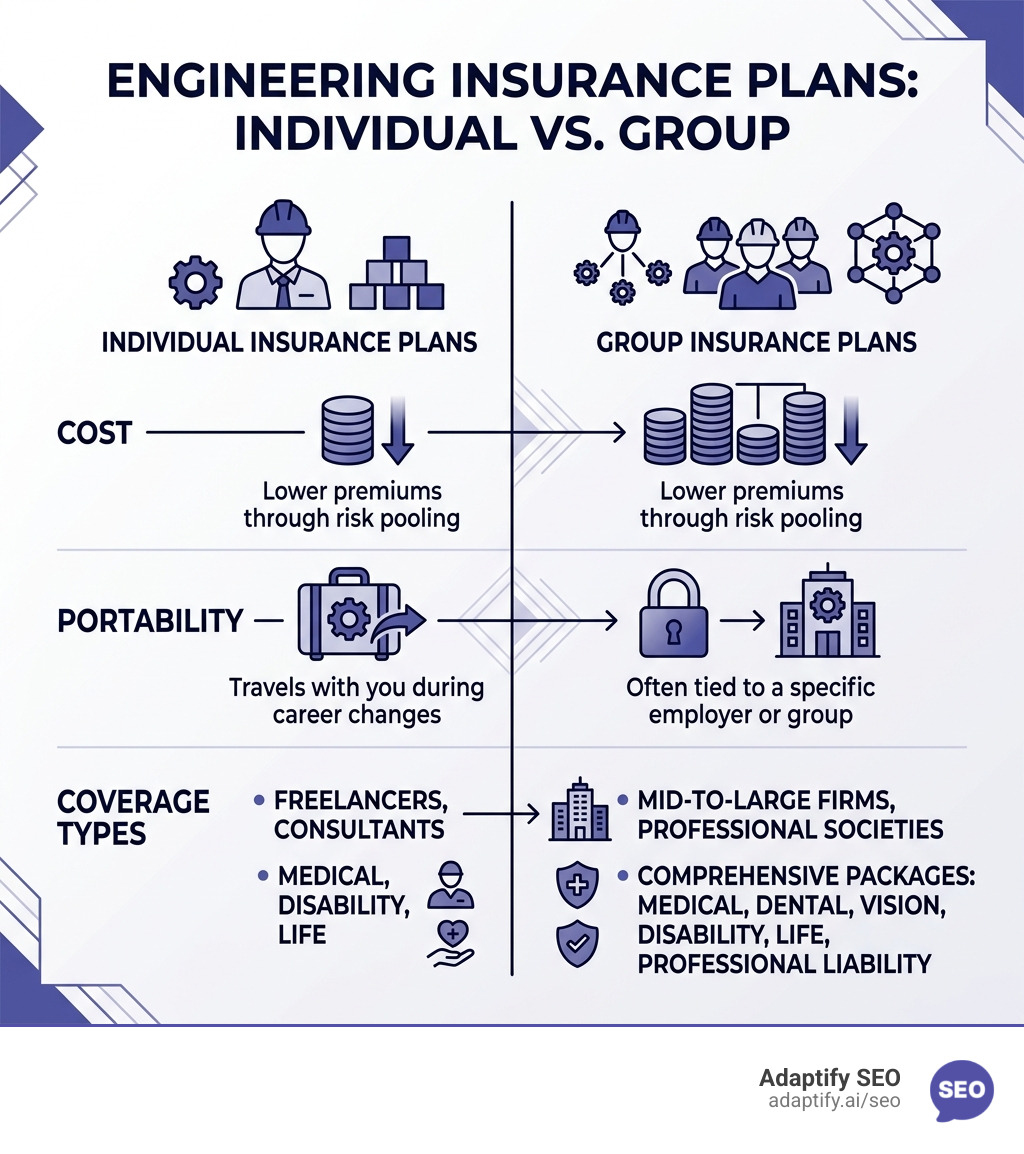

| Employer group plan | Engineers at mid-to-large firms | Lower premiums through risk pooling |

| Professional society plan | Members of ASCE, IEEE, NSPE, AIChE | Group rates + portable coverage |

| Individual/marketplace plan | Freelancers or self-employed engineers | Flexibility, ACA subsidies possible |

| Small business group plan | Engineering firm owners | Tax credits, talent retention |

The challenge for engineers is career mobility. Many engineers change employers, go independent, or work across state lines. Standard employer-sponsored plans don't always travel with you. That's what makes professional society programs and portable group plans so valuable for this field.

On top of medical coverage, engineers often need to think about:

Understanding how all these pieces fit together can save you significant money and prevent coverage gaps during career transitions.

I'm Hansjan Kamerling, a product designer and marketing consultant who has worked across SaaS, fintech, and data-driven platforms — industries where navigating health insurance for engineers and competitive benefits packages is a constant challenge for both individuals and small business owners. That hands-on experience with fast-moving, talent-driven teams shapes the practical approach you'll find throughout this guide.

One of the most significant perks of being a professional engineer is the collective bargaining power of your industry associations. Organizations like the American Society of Civil Engineers (ASCE), the Institute of Electrical and Electronics Engineers (IEEE), the National Society of Professional Engineers (NSPE), and the American Institute of Chemical Engineers (AIChE) don't just provide networking and technical standards; they act as massive risk pools.

By joining these societies, I've found that engineers can access insurance products that are often more robust and competitively priced than what they could find on the open individual market. For instance, Health | ASCE Member Insurance offers a suite of products ranging from major medical to niche coverages like high-limit accident insurance.

Similarly, the Insurance Benefits for IEEE Members & Engineers | IEEE program has been supporting its community for over 60 years. These programs are designed specifically with the engineering lifestyle in mind—addressing the fact that our work is often project-based and our careers are mobile.

The biggest "pain point" I see for engineers is the fear of losing coverage during a job change or when starting a solo consultancy. Traditional employer-sponsored health insurance is tied to the company. When you leave, you’re often stuck with expensive COBRA premiums or the stress of finding a new plan in a tight window.

Portable insurance solves this. Programs like the IEEE Member Group Insurance Program, administered by AMBA, provide coverage that belongs to you, not your boss. Whether you move from a big firm to a startup or take a six-month sabbatical to travel, your policy stays active as long as you maintain your membership.

AIChE members also benefit from this portability through the Aon-Stride Health Exchange. This platform allows chemical engineers to browse Member Only Insurance Products that include cancer insurance, disability, and dental plans that transition seamlessly between career stages.

The math behind these plans is simple: strength in numbers. When an insurance carrier sees 57,000 IEEE members insured through a single program, they are willing to offer lower group rates that an individual could never negotiate alone.

These societies often negotiate "lock-in" periods that provide long-term financial stability. For example, AIChE offers term life insurance with coverage up to $2,000,000, where members can lock in their rates for up to 20 years. This is a massive advantage for young engineers looking to protect their families at a low cost while they are healthy.

Furthermore, firms can benefit directly. At the Insurance | National Society of Professional Engineers (NSPE), engineering firms may qualify for an underwriting premium credit of up to 5% if at least half of their professional staff are NSPE members. It’s a rare "win-win" where professional development leads directly to lower overhead costs.

If you’re running a small engineering firm in April 2026, you know that the "war for talent" is real. You aren't just competing with the firm down the street; you're competing with tech giants and global consultancies. Offering a high-quality health insurance for engineers package is often the deciding factor for a candidate.

According to research, 66 percent of small business respondents offer health insurance specifically because it helps them hire and retain the best workers. In the engineering world, where specialized skills are at a premium, this isn't just a benefit—it's a survival strategy.

Several factors influence what your firm will pay for a group plan:

Beyond just "keeping people happy," there are hard financial reasons to offer group coverage. Small businesses with 25 or fewer full-time equivalent employees may qualify for the Small Business Health Care Tax Credit, provided they pay at least 50% of the employee premium costs.

Using resources like Small Business Health Insurance for Engineering Firms | eHealth allows firm owners to compare plans side-by-side. For a small firm, providing these benefits creates a "recruitment edge" that allows you to punch above your weight class. It signals to potential hires that your firm is stable, professional, and cares about its people.

If you are looking to grow your firm's digital presence to match your professional reputation, you can find more info about SEO content strategies to help your practice stand out online.

Choosing the right "alphabet soup" of plan types is critical. Engineers tend to be analytical, so I like to break these down by their mechanical differences:

| Plan Type | Flexibility | Cost | Network Rules |

|---|---|---|---|

| HMO (Health Maintenance Organization) | Low | Lowest | Must stay in-network; need referrals for specialists. |

| PPO (Preferred Provider Organization) | High | Highest | Can see any doctor; no referrals needed; out-of-network covered at higher cost. |

| POS (Point of Service) | Medium | Moderate | Hybrid; usually requires a Primary Care Physician but allows out-of-network visits. |

Interestingly, POS plans have become a staple for small engineering offices. Data from eHealth shows that POS plans account for nearly half (47 percent) of the small business plans selected by customers.

Why? Because engineers often value a balance of logic and flexibility. POS plans offer the lower costs associated with an HMO-like core network but provide a "safety valve" that allows employees to see out-of-network specialists if they are willing to pay a bit more. For a firm with employees who might live in different suburbs or travel for projects, this middle ground is often the "sweet spot."

For firms that can afford higher premiums, PPO plans are the gold standard for talent attraction. If your lead structural engineer has a specific specialist they've seen for years, a PPO ensures they can keep that relationship without jumping through hoops. In a high-stress profession, removing the friction of "referrals" and "network restrictions" is a highly valued luxury.

In my experience, many engineers confuse "health insurance" with "professional protection." While your medical plan covers your body, it does nothing for your career if a design error leads to a lawsuit. A complete "wellness" blueprint for an engineer must include both.

Professional Liability Insurance (also known as Errors and Omissions or E&O) is essential. While health insurance covers your appendectomy, E&O covers the legal costs if a bridge you designed develops cracks or a software system you engineered fails.

Providers like Victor Insurance work closely with societies like NSPE to offer specialized business insurance. They even provide risk management resources—like contract reviews and webinars—to help you avoid claims in the first place. This is a critical distinction: health insurance is reactive (it pays when you're sick), whereas professional liability combined with risk management is proactive.

To understand how to build a strong foundation for your firm’s online authority, check out more info about SEO backlinks.

Professional societies also fill the gaps that standard health plans leave behind. These include:

Navigating the enrollment process doesn't have to be a manual calculation exercise. Several digital tools and specialized brokers cater specifically to the engineering community:

If you are an agency owner looking to scale your business by offering these types of specialized insights to your clients, you might explore more info about SEO white label services to enhance your service offerings.

Beyond insurance, engineering societies provide a "toolkit" for small business owners. When you enroll in an Associate Partner program (like the one offered by ASCE for firms with 10 or more engineers), you gain access to:

Societies act as a "large group" negotiator. By pooling thousands of members together, they can secure lower rates from insurance carriers (like New York Life or Lloyd's of London) that an individual or small firm could never get on their own.

If you are on a standard employer-sponsored plan, usually no (though you may have COBRA rights). However, if you have a plan through a professional society like IEEE or AIChE, your coverage is portable. It follows you from job to job as long as you remain a member.

Health insurance covers your personal medical expenses. Professional liability (E&O) insurance covers your business against claims of negligence, errors, or omissions in the engineering services you provide. You need both to be fully protected.

Securing the right health insurance for engineers requires a bit of that analytical mindset we're known for. By leveraging professional societies, understanding the flexibility of POS and PPO plans, and ensuring your professional liability is as robust as your medical coverage, you can build a safety net that supports both your health and your career.

At Adaptify SEO, we understand the value of precision and automation. Just as you use engineering principles to solve complex physical problems, we use AI-driven, automated SEO services to solve the complex problem of digital visibility. We help agencies streamline their strategy, content creation, and link building, allowing them to focus on high-level consulting while the "engine" of their SEO runs efficiently in the background.

Ready to engineer a better growth strategy for your business? Start your SEO journey with Adaptify and see how our comprehensive, automated solutions can enhance your efficiency and results.

Discover how medical SEO specialists elevate your practice with targeted strategies for local search, E-E-A-T, & patient growth.

Boost your real estate leads with Local SEO for real estate. Dominate Google Maps, outrank portals & master GBP in 2026!

Master SEO by learning how to do keyword research. Discover intent, find valuable keywords, analyze metrics, and choose the right tools.

Join 1,000+ agencies already delivering SEO and AI visibility from a single platform without increasing their headcount.Join 1,000+ agencies already delivering SEO and AI visibility from a single platform without increasing their headcount.